The luxury segment of the real estate market has entered a phase of stabilization in 2026. The national entry point to the luxury market, defined as the top 10% of listings, has leveled out, holding steady near $1.2 million, which represents a fractional 0.6% decline from the previous year.

While entry-level luxury has found a reliable floor, the ultra-luxury segment (the top 1% of the market) is showing signs of renewed momentum. Although the threshold for the top 1% of listings remains slightly lower than it was a year ago, it has climbed consistently for five consecutive months, rising from $5.4 million in September 2025 to $5.6 million to start 2026. This sustained momentum suggests that while the broader high-end market is normalizing, the most exclusive properties are regaining ground and continue to command premium pricing, a trend expected to continue in 2026.

The share of listings priced at $1 million or more expanded dramatically over the past several years, rising from 7.4% in 2017 to a peak of 14.1% in 2024. In 2025, that share has moderated slightly to 13.2%, signaling stabilization rather than reversal. The rapid repricing that defined the post-pandemic housing boom has given way to a more measured environment, where seven-figure homes remain far more common than they were pre-2020, but price acceleration has cooled. The luxury segment has moved from expansion to normalization.

(Top 50 Metros by Population)

Luxury housing remains highly concentrated geographically. While 12.0% of listings nationally are priced at $1 million or more, that share varies dramatically across major metros. More than half of listings in Los Angeles exceed the million-dollar threshold, while San Francisco, Boston, and New York each see roughly one-third or more of inventory in seven-figure territory. Miami has firmly established itself as a leading luxury hub as well, with more than one in five listings priced above $1 million. In contrast, large Sun Belt and Midwest markets remain in the single digits. The data reinforce that luxury real estate in 2026 is not evenly distributed, but rather deeply tied to concentrated wealth centers and constrained coastal supply.

Legacy Luxury and Emerging Markets

One of the most defining macro trends of 2026 is the structural shift in where luxury inventory is accumulating. For the better part of a decade, New York consistently held the nation’s largest inventory of million-dollar homes. However, in a major geographic realignment, the Miami metro officially surpassed New York by the end of 2025, boasting 10,513 active million-dollar listings compared to New York’s 9,216. This shift reflects not only a stronger inventory growth in Miami, but also relative scarcity in New York, which still maintains a higher share of million-dollar listings, as its absolute count has been surpassed.

This crossover is the culmination of a multi-year trend. Following the initial pandemic-era inventory contraction, Miami’s luxury market has seen a steady, persistent rise. While New York has slowly trended upwards, it has not expanded at the same pace as Miami since 2022. This divergence reflects a mature New York market where high-end inventory remains sizable but slower to expand, compared to Miami’s rapidly deepening, year-round luxury supply base.

Insulated from the lock-in effect

For four years, the broader U.S. housing market has been gripped by a “lock-in effect,” where homeowners with low mortgage rates have chosen not to sell. However, the luxury housing market operates by a different set of rules.

Luxury homebuyers, especially those in the market for properties $10 million and higher, are significantly less reliant on mortgage financing; as a result, these properties have outperformed and remain insulated from interest rate volatility. In premier global gateway markets like Miami, for example, cash transactions increasingly dominate as price points rise. Cash purchases account for 46.5% of homes priced between $1 million and $2 million, jumping to 64.4% for homes between $2 million and $5 million, and reaching a massive 84.7% for the $5 million to $10 million tier. Even for the most exclusive properties over $10 million, 60.9% are purchased with cash. Because financing isn’t a primary hurdle, sellers can afford to be patient, and buyers can transact swiftly when the right property becomes available.

Source: National Association of Realtors

Even as overall transaction volume remains subdued, million-dollar homes continue to account for a larger share of closed sales than in prior years. The segment now represents 7.5% of sales, up from 6.3% two years earlier. This sustained gain reflects both higher pricing thresholds and the relative financial resilience of high-end buyers. Luxury demand is no longer surging, but it continues to claim a disproportionate share of market activity, underscoring its insulation from many of the constraints facing mid-market buyers.

Demand and pacing reveal a fragmented landscape

While inventory normalizes, market balance indicators suggest that pacing isn’t uniform nationally. Time on the market for entry-level luxury homes (the 90th percentile) has normalized to a median of 92 days, up slightly from a year ago. Conversely, the ultra-luxury tier (the 99th percentile) is actually moving faster than it did last year, spending 108 days on the market (down 2 days YoY). Local conditions dictate speed: legacy tech hubs like San Jose are clearing luxury homes at a blistering pace, compared to much longer timelines in amenity-heavy resort and micropolitan markets.

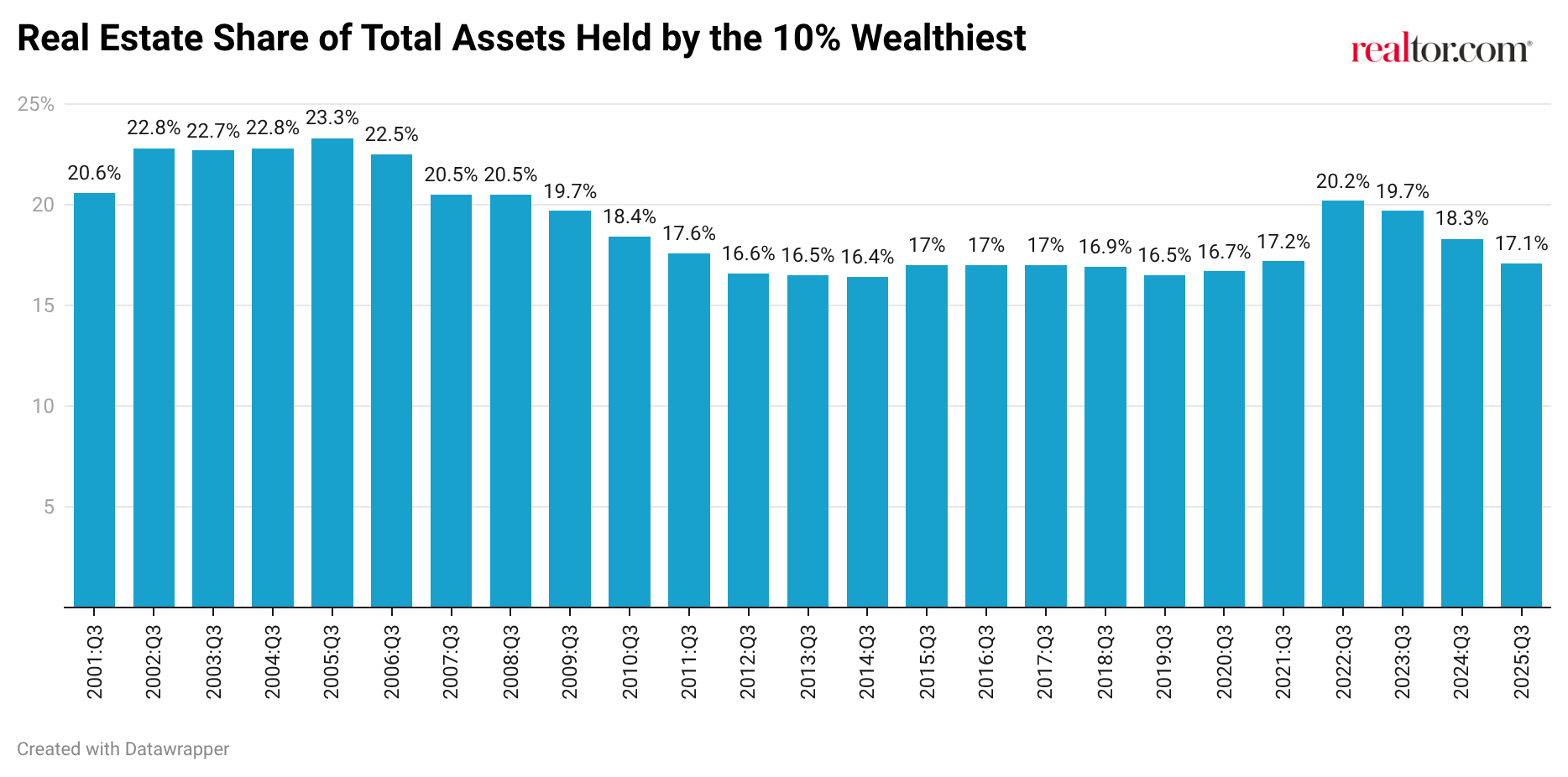

Real estate remains an important but not dominant component of wealthy households’ portfolios. In the latest data, real estate accounts for 17.1% of total assets among the top 10% of households, down from 20.2% in 2022 and well below the early-2000s peak above 22%. With real estate representing a smaller share of total wealth than in prior cycles, high-net-worth households retain meaningful flexibility in how they allocate capital. That balance sheet strength continues to provide structural support for luxury real estate demand, even in a more uncertain economic environment.

What’s ahead for the rest of 2026?

Looking forward, the luxury housing market is moving past the sharp volatility and post-pandemic recalibrations of recent years to find much firmer, stable ground. Nationally, the entry point for luxury has held steady at the start of the year, signaling that the broader luxury market has found a reliable baseline and reached a near-term floor.

However, beneath this national stabilization, the rest of the year will be defined by a more fragmented landscape in which select outlier metros continue to chart their own paths. For example, highly constrained legacy markets like Key West, FL, and emerging, amenity-rich micro-markets like Heber, UT, are still pushing luxury prices higher despite broader national cooling.

Ultimately, 2026 is shaping up to be a year of healthy normalization. Sellers are maintaining their pricing power by acting patiently, buyers are acting deliberately but with cash in hand, and the definition of where luxury lives in America continues to expand.

{kind=link}